You can Download Chapter 6 Cash Flow Statement Questions and Answers, Notes, 2nd PUC Accountancy Question Bank with Answers Karnataka State Board Solutions help you to revise complete Syllabus and score more marks in your examinations.

Karnataka 2nd PUC Accountancy Question Bank Chapter 6 Cash Flow Statement

2nd PUC Accountancy Cash Flow Statement NCERT Textbook Questions and Answers

2nd PUC Cash Flow Statement Short Answer Questions With Answers

Question 1.

What is a Cash Flow Statement?

Answer:

A Cash Flow Statement is a statement showing inflows and outflows of cash and cash equivalents from operating, investing and financing activities of a company during a particular period. It explains the reasons of receipts and payments in cash and change in cash balances during an accounting year in a company.

Question 2.

How are the various activities classified (as per AS-3 revised) while preparing cash flow statement?

Answer:

As per the Revised Accounting Standard 3 (AS-3), preparation of Cash Flow

Statement for each period is mandatory. AS-3 also specifies the classification of all inflows and outflows basically under the following heads:

- Cash Flow from Operating Activities

- Cash Flow from Investing Activities

- Cash Flow from Financing Activities

![]()

Question 3.

State the uses of cash flow statement?

Answer:

The uses of cash flow statement are as follows:

- It is useful for short term financial planning about inflows and outflow of cash

- It helps in analysing the reason for the change in cash and cash equivalent balances of a company

- It assists in determining and assessing liquidity and solvency positions of a company.

- It enables to analyse and study the trends of receipts and payments of cash from various activities of a company and thereby helps in drafting various policy measures and short term planning.

- It enables the segregation of cash flows from operating, investing and financing activities of the business separately.

- It assists in making decision about distribution of profit with reference to the availability of cash.

Question 4.

What are the objfectives of preparing cash flow statement?

Answer:

The important objectives for preparing Cash Flow Statement are as follows:

The most important objective that is fulfilled by preparing Cash Flow Statement is to ascertain the gross inflows and outflows of cash and cash equivalents from various activities.

Secondly, Cash Flow Statement helps in analysing various reasons responsible for change in the cash balances during an accounting year.

Cash Flow Statement also helps in ascertaining the requirement and availability of cash in near future.

This statement helps in analysing and understanding the liquidity and solvency of a company, thereby, depicting the true liquidity position to the Creditors and the investors.

Question 5.

Explain the terms Cash Equivalents and Cash flows.

Answer:

Cash equivalents: Cash equivalents are short term, highly liquid investments that are easily convertible into cash and which are subject to an insignificant risk of change in value. In other words, cash equivalents are held for the purpose of meeting short term cash commitments rather than for investment or any other purpose. An investment held for short-term maturity, say three months can be regarded as cash equivalent. Some examples of cash equivalents are treasury bills, commercial papers, etc.

Cash flows: cash flows are inflows and outflows of cash and cash equivalents.

A cash inflow results in increase in the total cash balance and a cash outflow results in decrease in the total cash balance.

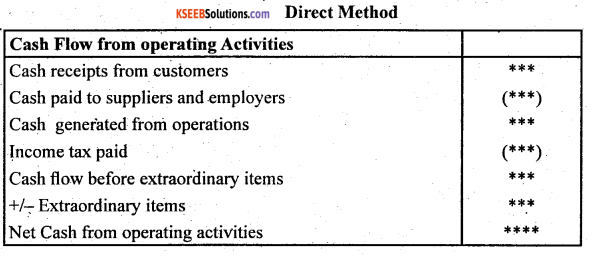

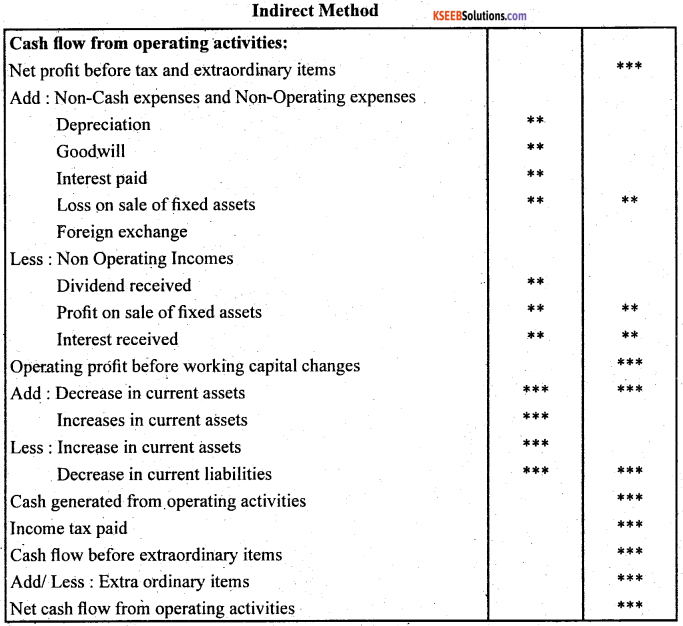

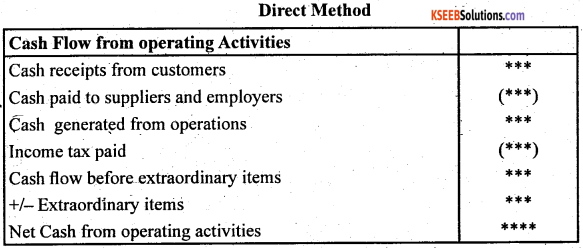

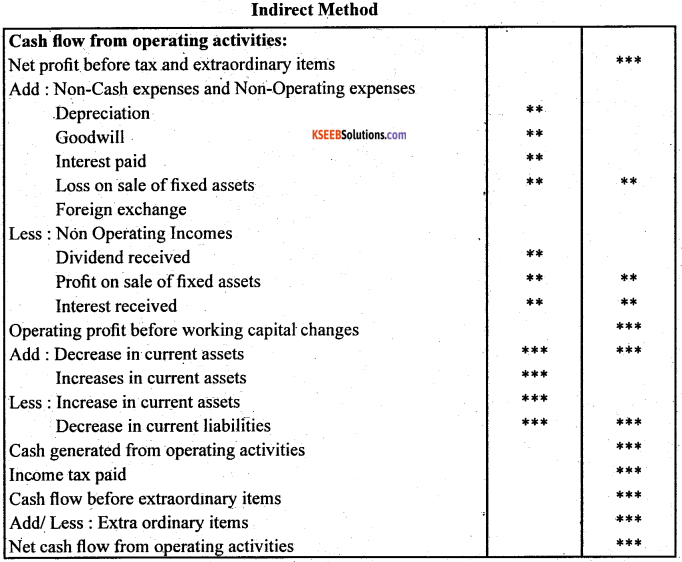

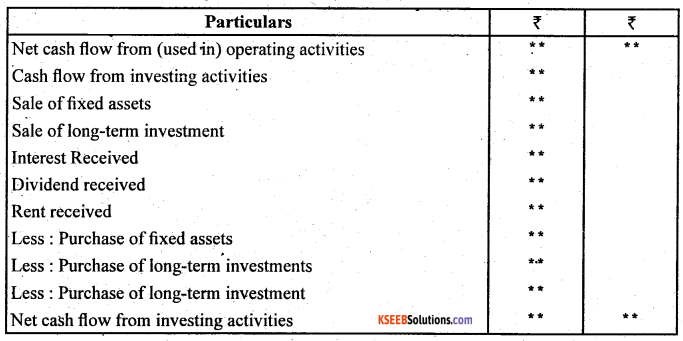

Prepare a format of cash flow from operating activities under direct method and indirect method.

![]()

Question 6.

Now that you know the meaning of operating activities, state clearly what would constitute the operating activities for the following types of enterprises?

(a) Hotel

(b) Film production house

(c) Financial enterprise

(d) Media enterprise

(e) Steel manufacturing unit

(f) Software business unit

Answer:

(a) Hotels

- Receipts from sale of goods to customer

- Payment pf wages and salaries, electricity, food items and other items used in accommodation

(b) Film production house

- Receipts from selling film rights of a film to the distributors

- Payment to the staff, actors, actresses, directors, etc.

(c) Financial enterprise

- Receipts from repayment of loans, interest incomes from investments; etc

- Repayments of loans, recovery expenditure for recover of loans etc, salaries of employees

(d) Media enterprise

- Receipts from advertisements

- Payments to staff, reporters, photographers, etc

(e) Steel manufacturing unit

- Receipts from sale of steel sheets, steel castings, steel rods, etc

- Payment for iron, coal, salaries to staff, etc

(f) Software business unit

- Receipts from sale of software and renewal of licenses

- Payment of salaries to their employees, etc

Question 7.

The nature/type of enterprise can change altogether the category into which a particular activity may be classified. Do you agree? Illustrate your answer.

Answer:

Yes, the nature or type of an enterprise can change altogether the category into which a particular activity may be classified. This can be better understood with the help of an example of two firms. One engaged in real estate and the other engaged in general business.

For the firm that is engaged in real estate business purchase and sales of building will be part of the operating activity on the other hand firm that is engaged in general business purchase and sales of building will be part of the investing activity. Hence it can be said that the classification of activities depends on the nature and type of enterprise.

2nd PUC Cash Flow Statement Long Answer Questions With Answers

Question 1.

Describe the procedure to prepare Cash Flow Statement.

Answer:

The procedure to prepare Cash Flow Statement is described in the following steps in their chronological order. ‘

Step 1: Ascertain the cash flows from operating activities

Step 2: Ascertain the cash flows from investing activities

Step 3: Ascertain the cash flows from financing activities

Step 4: Ascertain net increase or decrease by summing up the amounts of Steps 1, 2, and 3.

Step 5: Write the opening balance of cash and cash equivalents and deduct it from the amount ascertained in Step 4. The resulting figure arrived is the Closing Balance of Cash and Cash Equivalents.

Describe ‘Direct’ and ‘Indirect’ methods of ascertaining Cash Flow from Operating Activities.

As per the Accounting Standard 3 issued by the Institute of Chartered

Accountant of India, an enterprise should report cash flows from operating activities Using either of the following methods:

Direct Method: It represents the cash receipts from debtors (customers) and customers and cash payments to creditors (sellers) and employees. It

assists in estimating future cash flows. The excess of cash payments over cash.receipts is known as Net Cash Flow of Operating Activities.

Indirect Method: This method starts with the Net Profit before tax and extraordinary items. For this purpose, the Net Profit as revealed by the Profit and Loss Account cannot be taken into consideration as there exists some items which do not leads to outflow of cash. The following are those items that need to be added back to the Net Profit of the Profit and Loss Account.

![]()

Question 2.

Explain the major Cash Inflow and outflows from investing activities.

Answer:

Investing activities are those activities that are related to sales and purchases of long-term fixed assets like, land and building, plant and machinery, furniture, etc. These fixed assets are not held for resale. The activities like sale and purchase of investments that are not included in the cash equivalents are also included in investing activities. Any income arising from such investments (assets) are regarded a part of investing activities.

As per the AS3, the major cash inflows and outflows from investing activities are as follows:

(a) Cash payments to acquire fixed assets (including intangibles like, goodwill). These payments include capitalised cost of research and development and self-constructed fixed assets.

(b) Cash receipts from disposal of fixed assets (including intangible assets).

(c) Cash payments to acquire shares, warrants, or debt instruments of other enterprises and interest in joint venture (other than payments of those instruments consider as cash equivalents and are held for the trading purposes).

(d) Cash receipts from disposal of shares, warrants or debt instruments of other enterprises and interest from joint ventures (other than receipts from those held for trading purposes).

(e) Cash advances and loans made to third parties (other than advances, and loans made by financial enterprises). These will be treated as cash flows from the operating activities.

(f) Cash receipts from repayment of advances and loans made to third parties (other than advances and loans of financial enterprises). These will be treated as cash flows from operating activities.

(g) Cash receipts from insurance company for any property involved in accident.

(h) Any income arising from fixed assets or investments like interest, dividend, rent etc. In case of financial enterprises interest and dividend is treated as operating activities.

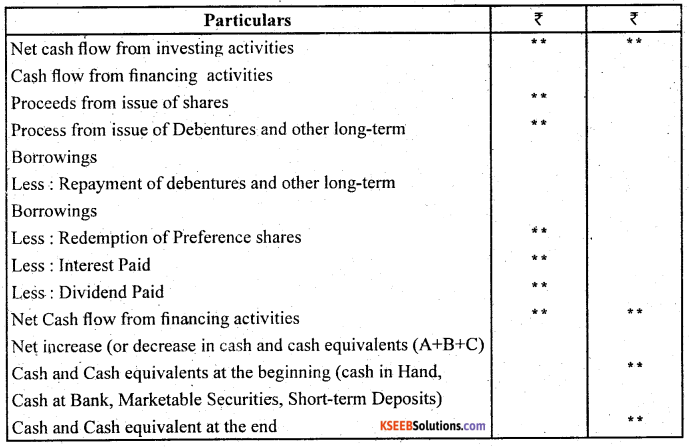

Question 3.

Explain the major Cash Inflows and outflows from financing activities.

Answer:

Financing activities are those activities that are related to capital or long term funds of an enterprise. These activities results in the change in the capital and borrowed funds.

As per the AS3, the major cash inflows from financing activities are as follows:

Cash proceeds from issue of shares and other similar instruments.

Cash proceeds from issue of debentures, loans, notes, bonds, and other short and long-term borrowings.

As per the AS3, the major cash outflows from financing activities are as follows: Cash repayments of the amount borrowed in form of debentures, loans, notes bonds, and other short and long-term borrowings.

Buy-back of shares and debentures.

Interest paid on debentures, loans, and advances.

Dividend paid to the preference shareholders and equity shareholders.

An important point that must be noted is that the purchase and sale of securities, interest paid or received and dividend received is treated as cash flow from operating activities for an investment company. But dividend paid is treated as cash flow from financing activities.

2nd PUC Cash Flow Statement Numerical Questions

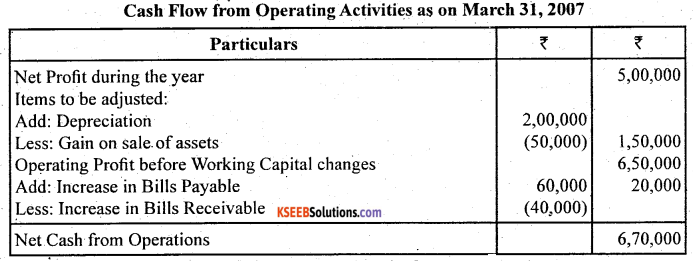

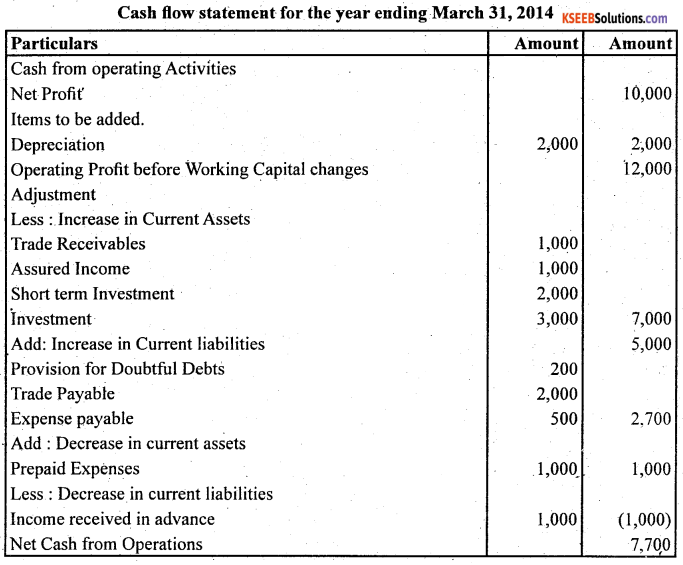

Question 1.

Anand Ltd., arrived at a net income of ₹ 5,00,000 for the year ended March 31, 2014. Depreciation for the year was ₹ 2,00,000. There was a profit of ₹ 50,000 on assets sold which was transferred to Statement of Profit and Loss account. Trade Receivables. increased during the year ₹ 40,000 and Trade Payables also increased by ₹ 60,000. Compute the cash flow from operation activities by the indirect approach.

Answer:

![]()

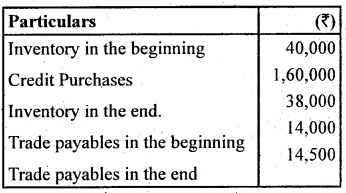

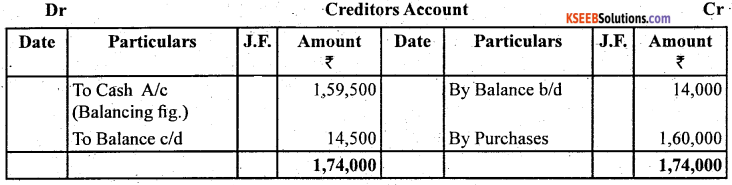

Question 2.

From the information given below you are required to calculate the cash paid for the inventory:

Answer:

Question 3.

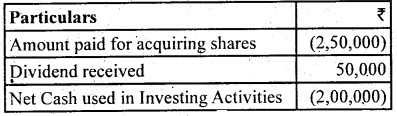

For each of the following transactions, calculate the resulting cash flow and state the nature of cash flow, viz., operating, investing and financing.

(a) Acquired machinery for ₹ 2,50,000 paying 20% by cheque and executing a bond for the balance payable.

(b) Paid ₹ 2,50,000 to acquire shares in Informa Tech, and recti da dividend of ₹ 50,000 after acquisition;

(c) Sold machinery of original cost ₹ 2,00,000 with an accumulated depreciation of ₹ 1.60.0 for ₹ 60,000.

Answer:

(a) Part payment ₹ 50,000 for acquiring machinery ₹ 2,50,000 is related with Investing Activities

(b)

Amount paid to acquire assets and dividend received is a part of Investing Activities.

(c) Inflow of cash of ₹ 60.000 on sale of machinery is a part Investing Activities.

Question 4.

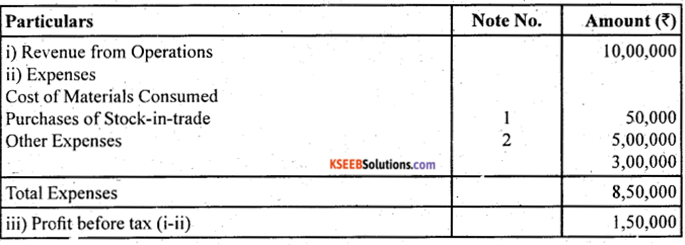

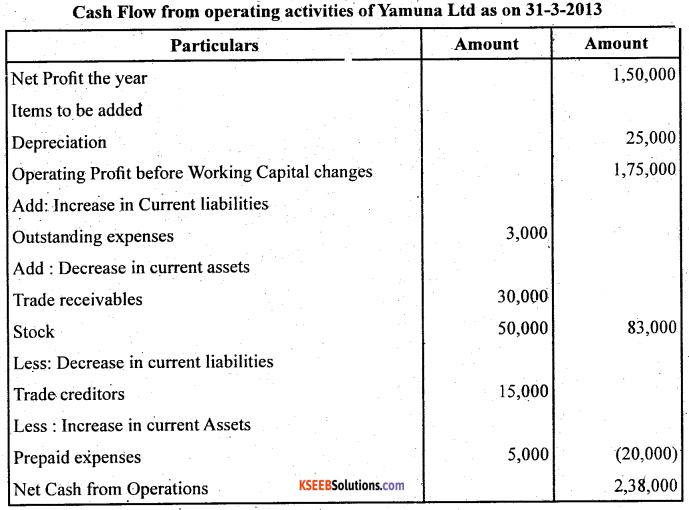

The following is the Profit and Loss Account of Yamuna Limited:

Statement of Profit and Loss of Yamuna Ltd., for the year ended March 31, 2015

Additional information:

- Trade receivables decrease by ₹ 30,000 during the year.

- Prepared expenses increase by ₹ 5,000 during the year.

- Trade payables increase by ₹ 15,000 during the year.

- Outstanding Expenses payable increased by ₹ 3,000 during the year.

- Other expenses included depreciation of ₹ 25,000.

Compute net cash from operations for the year ended March 31, 2014 by the indirect method.

Answer:

![]()

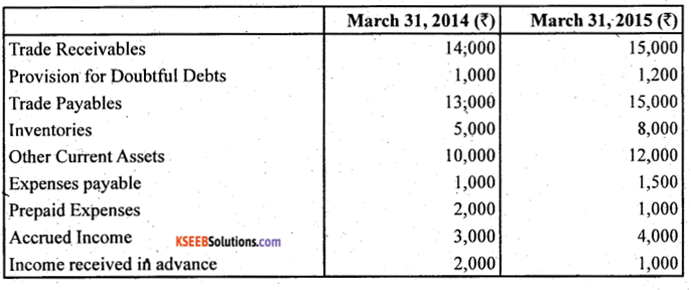

Question 5.

Compute cash from operations from the following figures:

- Profit for the year 2014-15 is a sum of ₹ 10,000 after providing for depreciation of ₹ 2,000

- “The current assets of the business for the year ended March 31, 2014 and 2015 are as follows:

Answer:

Question 6.

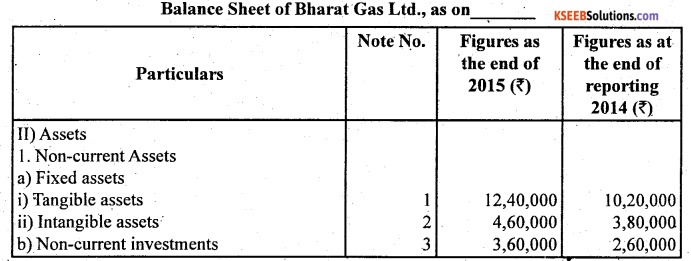

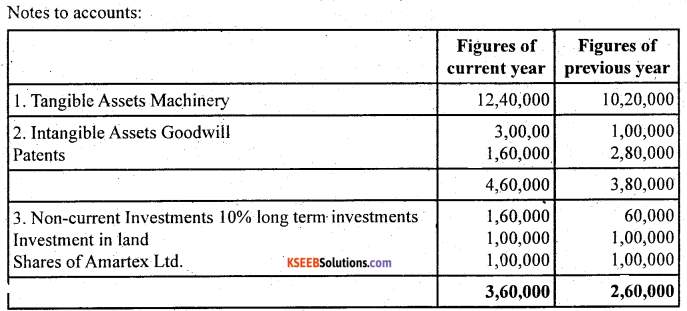

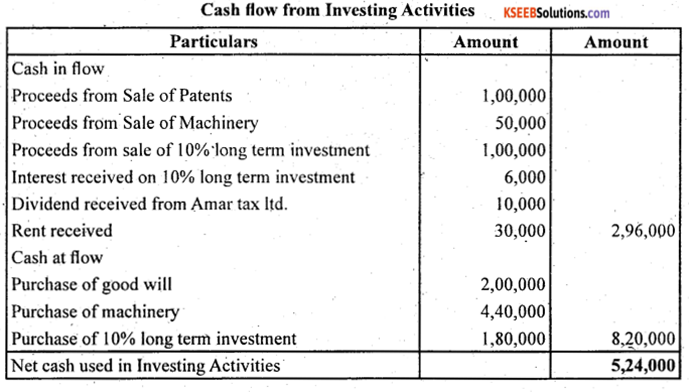

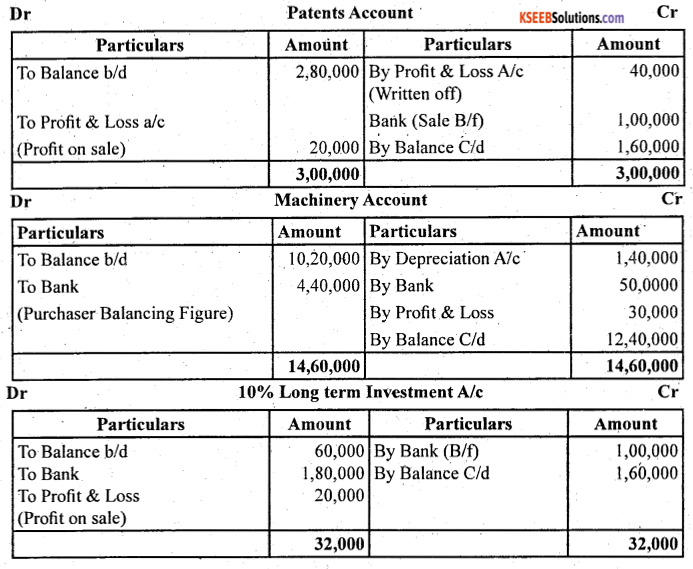

From the following particulars of Bharat Gas Limited, calculate cash flows from Investing Activities. Also show the workings clearly Preparing the ledger accounts:

Balance Sheet of Bharat Gas Ltd., as on

Notes:

- Tangible assets Machinery

- Intangible assets = Patents

Additional Information:

(a) Patents were written-off to the extent of ₹ 40,000.and some a profit of ₹ 20,000.

(b) A Machine costing ₹ 1,40,000 (Depreciation provided there on ₹ 60,000) was sold for ₹ 50,000. Depreciation charged during the year was ₹ 1,40,000.

(c) On March 31, 2014, 10% Investments were purchased for ₹ 1,80,000 and sonic Investments were sold at profit of ₹ 20,000. Interest on Investment was received on March 31, 2015.

(d) Amartax Ltd. paid Dividend @ 10% on its shares.

(e) A plot of land had been purchased for investment purposes and let out for commercial use and rent received ₹ 30,000.

Answer:

![]()

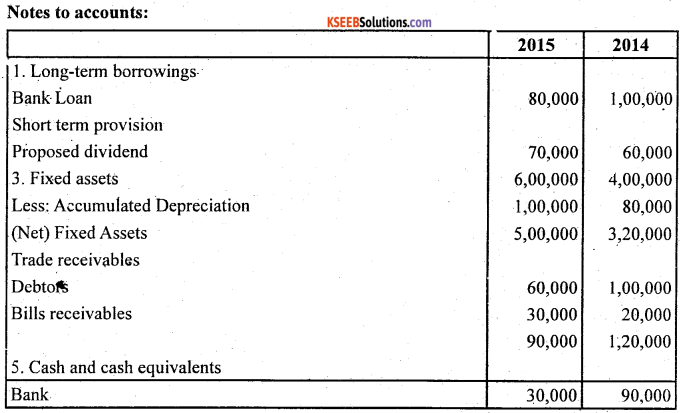

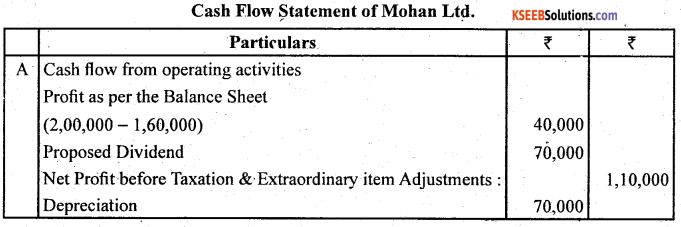

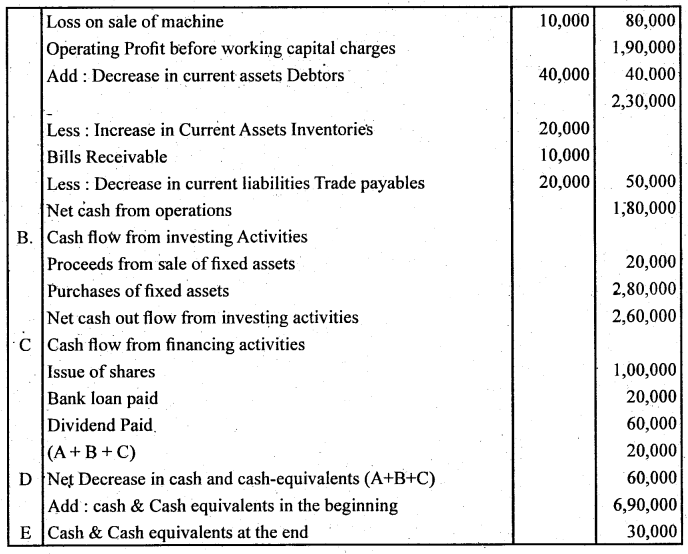

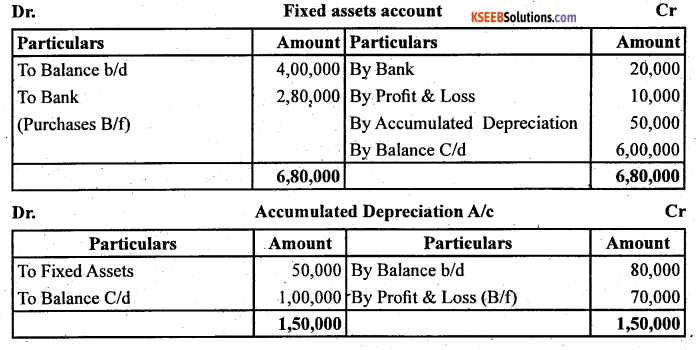

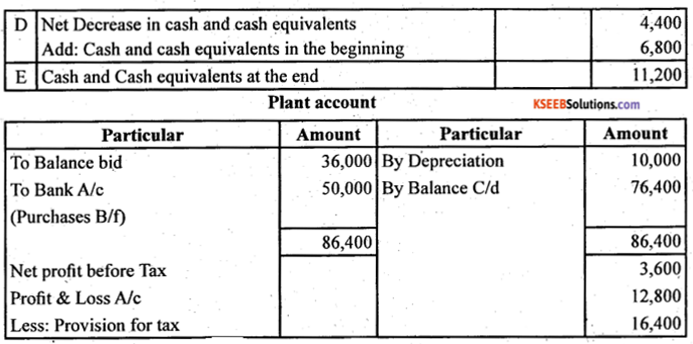

Question 7.

From the following Balance Sheet of Mohan Ltd., prepare cash Balance Sheet of Mohan Ltd., as at 31st March 2014 and 31st March 2015 flow Statement:

Additional Information:

Machine Costing ₹ 80,000 on which accumulated depreciation was Rs. 50,000 was sold for ₹ 20,000.

Answer:

![]()

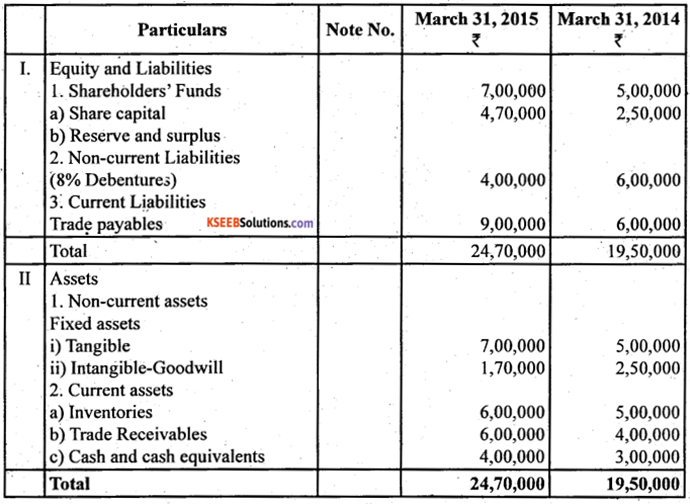

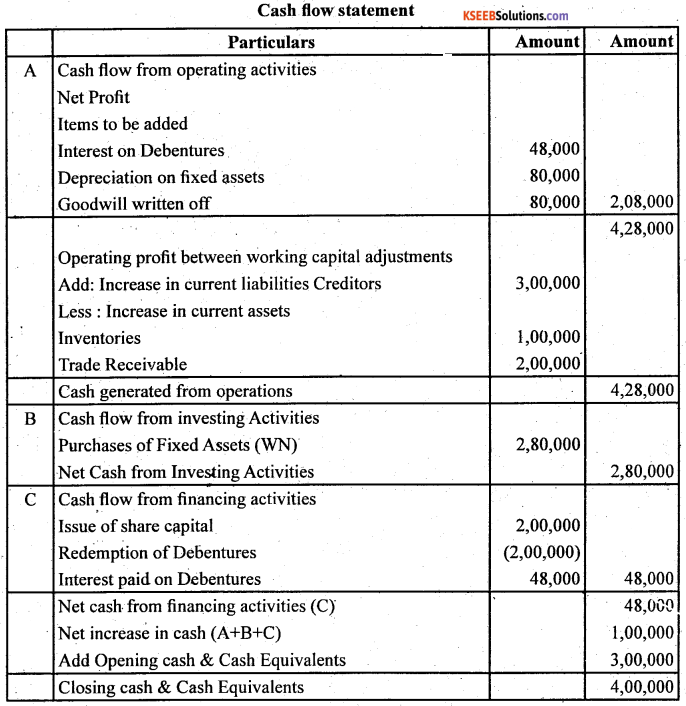

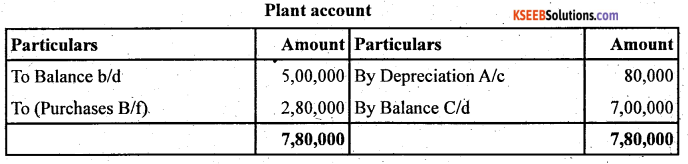

Question 8.

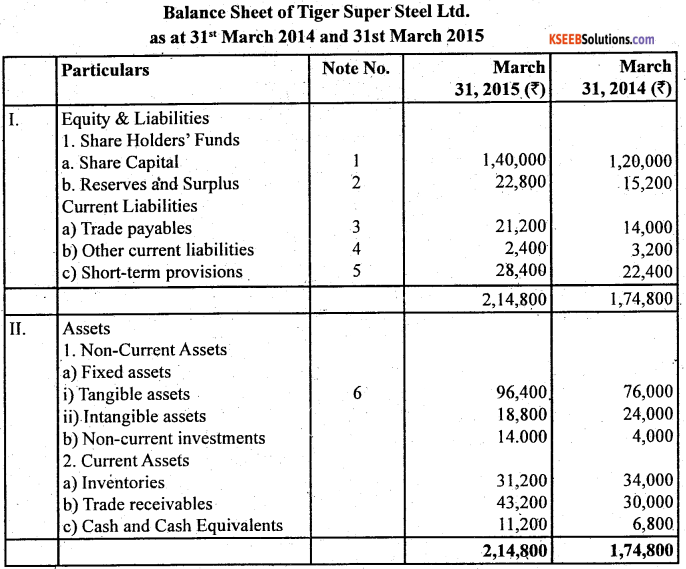

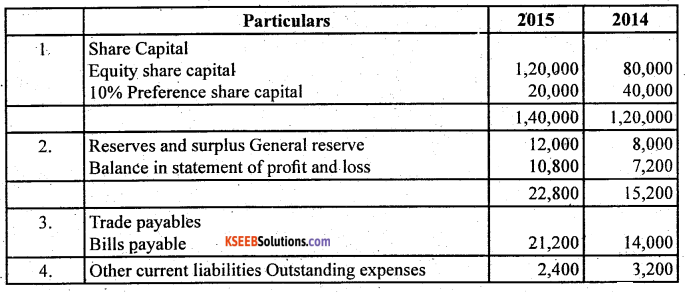

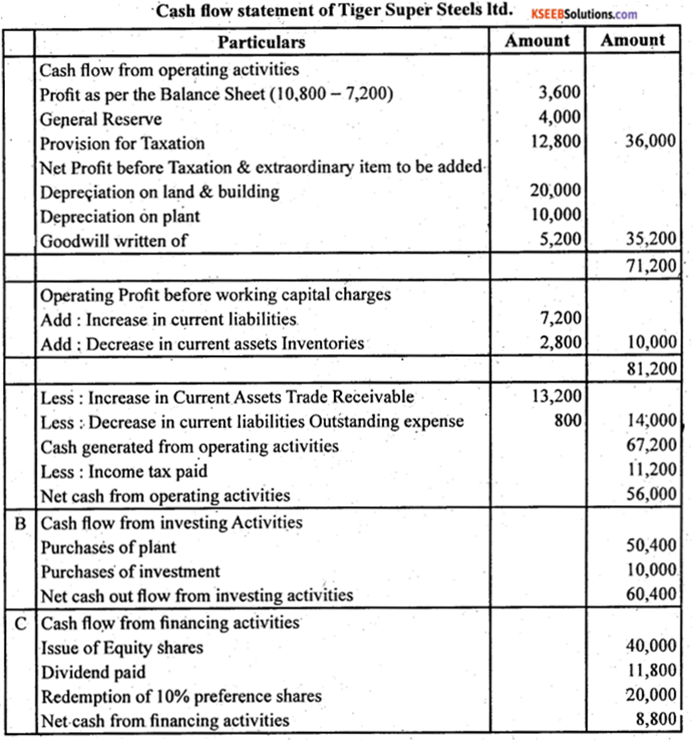

From the following Balance Sheets of Tiger Super Steel Ltd., prepare Cash Flow Statement:

Notes to accounts:

Additional Information: Depreciation Charge on Land & Building ₹ 20,000, and Plant ₹ 10,000 due the year.

Answer:

Question 9.

From the following information, prepare cash flow statement:

Answer:

Question 10.

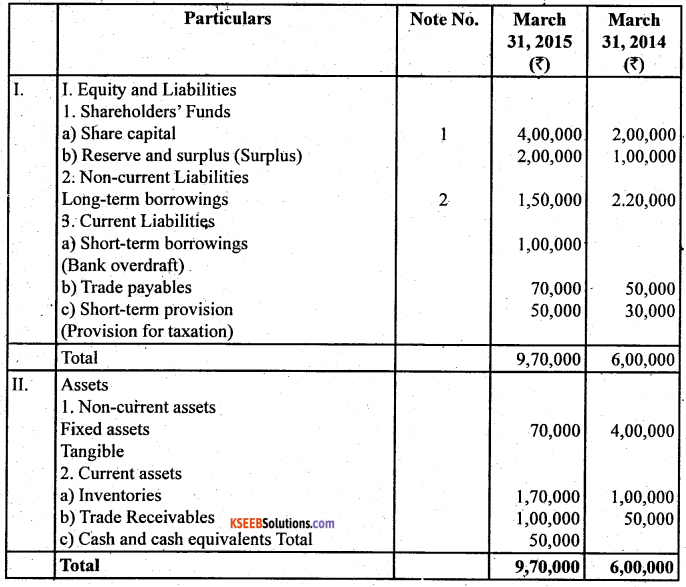

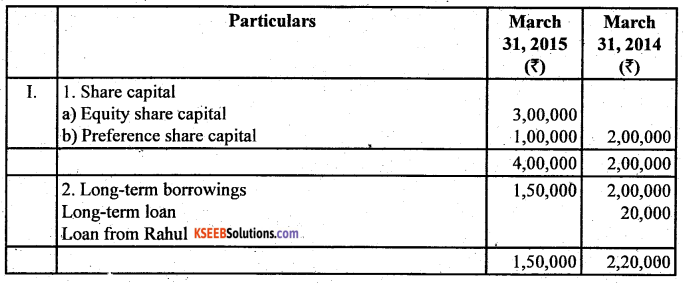

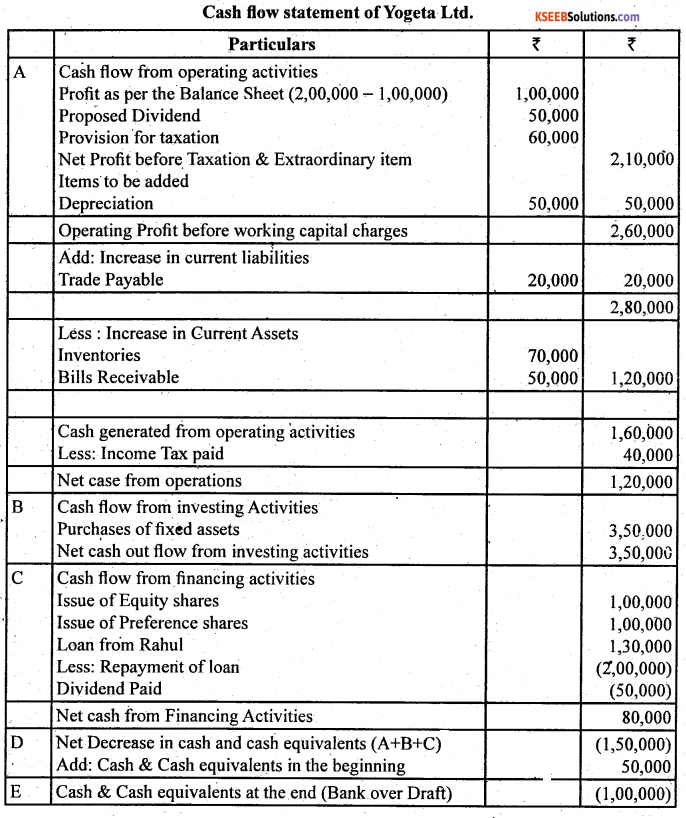

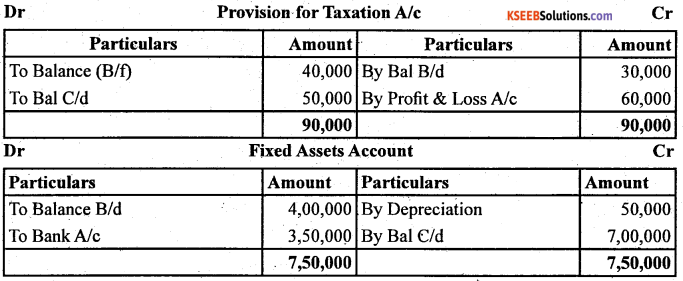

From the following Balance Sheet of Yogeta Ltd., prepare cash flow statement:

Notes of accounts:

Additional Information: Net Profit for the year after charging ₹ 50,000 as Depreciation was ₹ Dividend paid on Share was ₹ 50,000, Tax Provision created during the year amounted to Rs 60,000.

Answer:

![]()

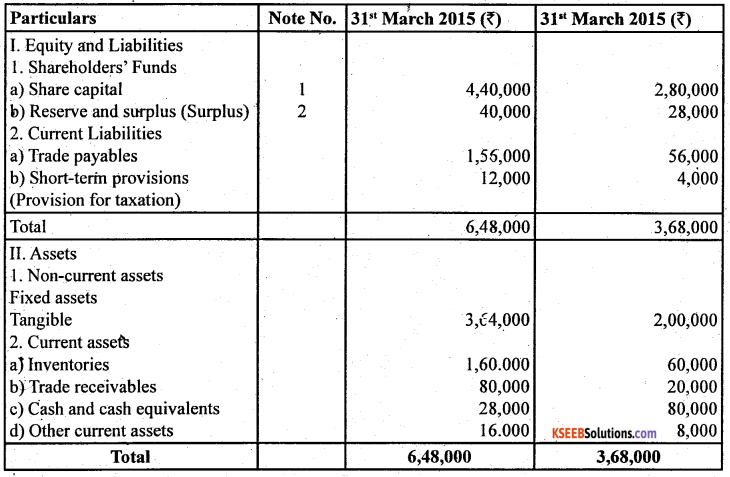

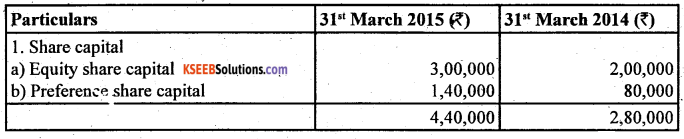

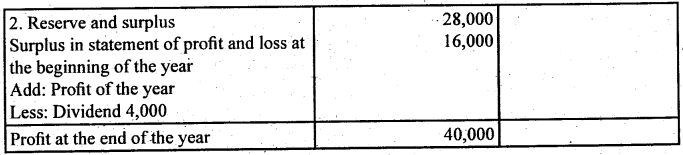

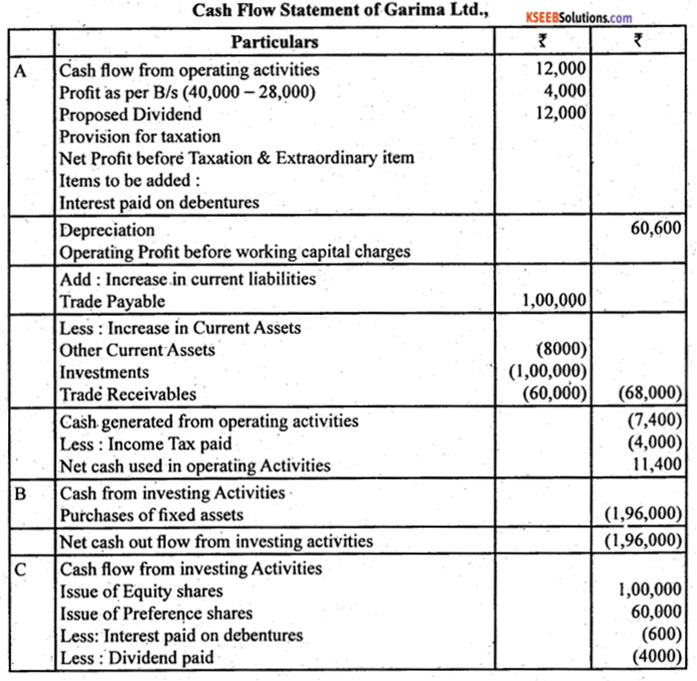

Question 11.

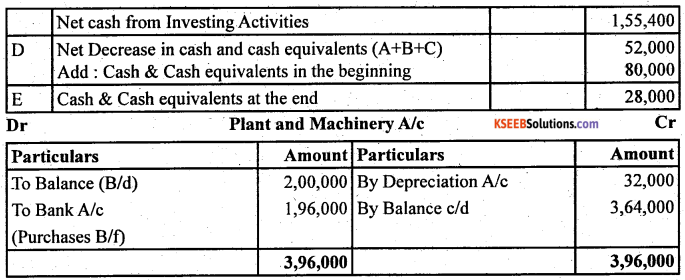

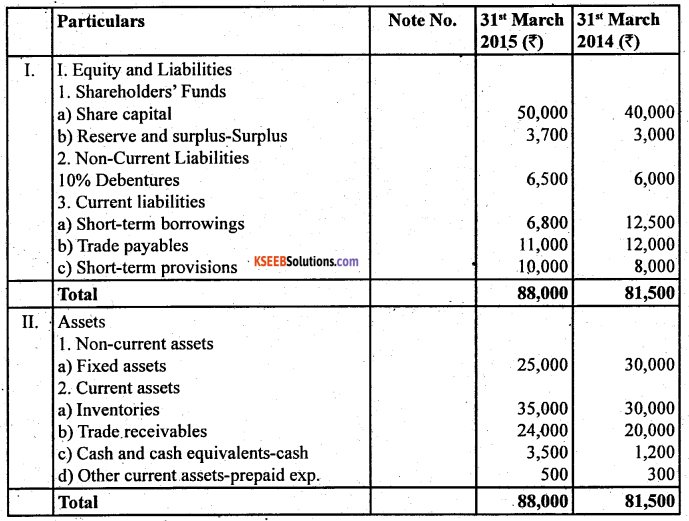

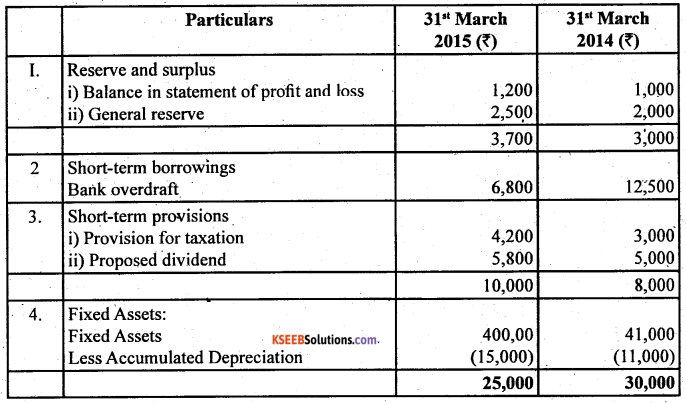

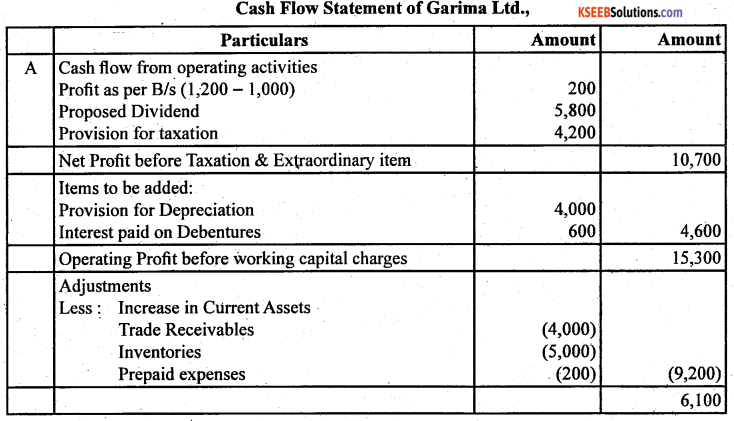

Following is the Financial Statement of Garima Ltd., Prepare cash flow statement.

Notes to accounts:

Additional Information:

1. Interest paid on Debenture ₹ 600

2. Dividend paid during the year ₹ 4,000

3. Depreciation charged during the year ₹ 32,000

Answer:

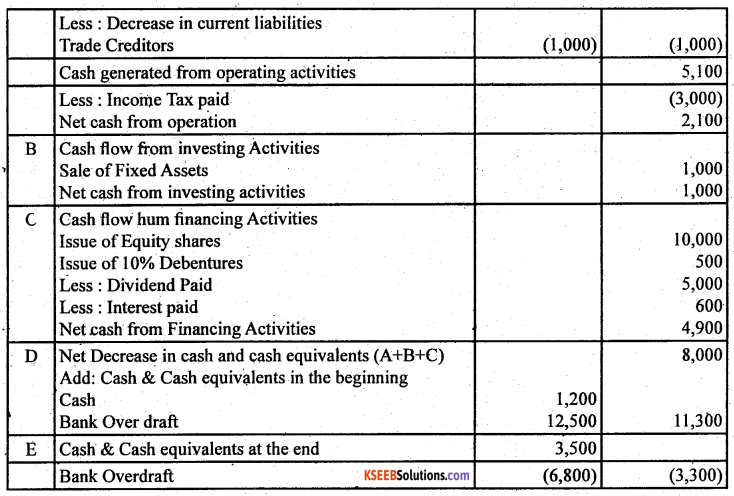

Question 12.

From the following Balance Sheet of Computer India Ltd., prepare cash flow statement.

Notes to accounts:

Additional Information:

Interest paid on Debenture ₹ 600

Answer:

![]()